Reporter

Nearly three weeks ago, Kimberly Minnick’s parents received a letter from her health insurance company.

“My mom called me to say my health insurance was ending and that I’d need to get a physical before the end of the year,” Minnick said.

According to the 24-year-old Truett Seminary student, Celtic Insurance Co. was going out of business.

Minnick said she’s lost her insurance providers before. “It’s the third time that’s happened to me,” she said.

Minnick’s parents health insurance plan hasn’t covered her for the last six years because she has hypothyroidism – pre-existing health condition.

A pre-existing health condition is a medical issue an individual has to live with, or one that is known of and will become a treatable issue in the future. They are often considered a liability for insurance providers. Consequently, many insurance companies are slow to offer coverage policies to people who may be that sort of liability.

Celtic offered Minnick a health plan she could qualify for despite her health issue.

“The medicine I need has bovine in it,” Minnick said. “So I take the off brand which contains a synthetic substitute.” Minnick, in addition to having a preexisting condition, is also a vegan.

There has been a federally sponsored insurance plan available to people with pre-existing conditions. The Pre-existing Condition Insurance Program will end this December, as decided by the Affordable Care Act.

When asked about how she thought the Affordable Care Act would influence how she picked a new insurance provider, Minnick said, “I don’t know.”

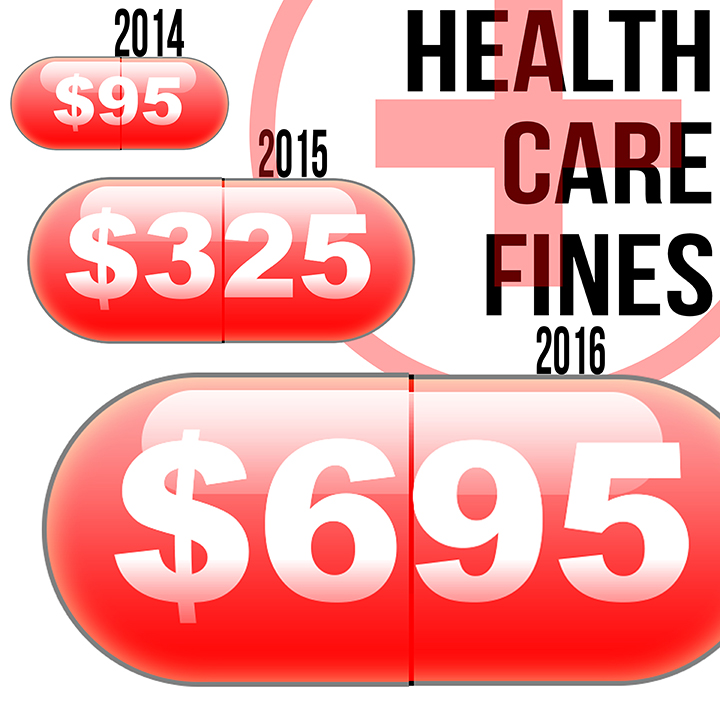

Minnick has until the end of the year to decide on a new health insurance plan or face a $95 fine after open enrollment ends in March. Beyond that, she said, there’s not much more she understands about the legislation.

“We tried to get on the Affordable Care Act website, but it was down,” Minnick said. “I need to learn more about the Affordable Care Act.”

The Affordable Care Act mandates that everyone, with a few exceptions, must have health insurance.

There is a fine for not complying with the law. It is calculated by income percentage or by charging a dollar amount per uninsured person, per household. People are given whichever total is greater.

The fine will be raised from $95 to $325 dollars per uninsured person in 2015 or from 1 to 2 percent of a household’s income. Then it increases to $695 per person or 2.5 percent of a household’s income by 2016. After that the fines will be adjusted for inflation and continue to increase annually.

Betty Fornelius is the insurance claims coordinator for the Baylor University Student Health Insurance Plan, a BlueCross BlueShield of Texas policy offered to Baylor students.

“Know your plan,” she said. “Know what you’re buying.”

Health insurance, like car insurance, is a service for making expensive fixes and procedures more affordable. For a monthly or yearly fee called a premium, a health insurance company agrees to cover a portion of a buyer’s medical expenses.

“Nothing’s free,” Fornelius said. Consumers may expect to pay larger premiums for more coverage options. Premiums are for the insurance company to decide, though customers often have options that mean bigger or smaller premiums.

A deductible is the amount of a bill the buyer must pay in order for the insurance coverage to kick in.

Once a patient has met the deductible amount, the insurance company will split the remainder of the bill with their client. By paying a large percentage of the bill, the company leaves a balance amount the patient is responsible to pay. For example, if the company pays 80 percent, the patient is left to cover remaining 20 percent. That’s called co-insurance.

If the customer is paying less in co-insurance, the company is responsible for more of the bill. Fornelius said smaller co-insurance rates also drive up premium costs.

Co-pay is expected from a patient for certain medical expenses such as doctor’s office visits. It’s a discounted price that’s paid for out-of-pocket and is never applied to the deductible.

The Affordable Care Act is complex, but there are two aspects of healthcare coverage it operates around — insurance companies and the people who buy from them.

Minnick’s story is an example of something the Affordable Care Act was written to fix.

The act, which was signed into law March 23, 2010, prohibits insurance companies from denying coverage or charging more to people like Minnick because of their pre-existing conditions. Also, it specifically prohibits company or group insurance policies from writing off an employee’s dependents with pre-existing health conditions. Coverage provided by an employer cannot leave out a person’s dependents such as children or spouses because of illnesses or pre-existing conditions. Coverage must be available to dependents until their 26th birthday.

According to the healthcare exchange website that was created under the new law, there is an exception for plans purchased individually — not through an employer — before March 2010. Those “grandfathered” plans can still keep people with pre-existing conditions out. Such plans are not available within the Health Insurance Marketplace.

The Marketplace is a federally endorsed website that uses an uninsured client’s non-medical information to list what insurance plans are available to them by state, region and income.

It is not the only way to purchase coverage. Under the law, employers must provide a policy to their full-time employees. Private health policies are available for sale to individuals, outside the Marketplace.

All the coverage options from the Marketplace meet a criterion of coverage. They provide for preventative care. And offer coverage for pre-existing conditions and “essential medical benefits” like emergency room visits and pediatric services.

The Marketplace considers a person’s eligibility for Medicaid and Children’s Health Insurance Program, federal health coverage, and whether or not a person qualifies for special “cost sharing reduction” plans or even tax-credits to help the cost of affording a new plan.

Minnick has some things to think about before deciding on a replacement provider. In light of the Affordable Care Act, there are fiscal penalties weighing on the issue and a number of regulations and provisions that will make insurance shopping different than it’s been before.